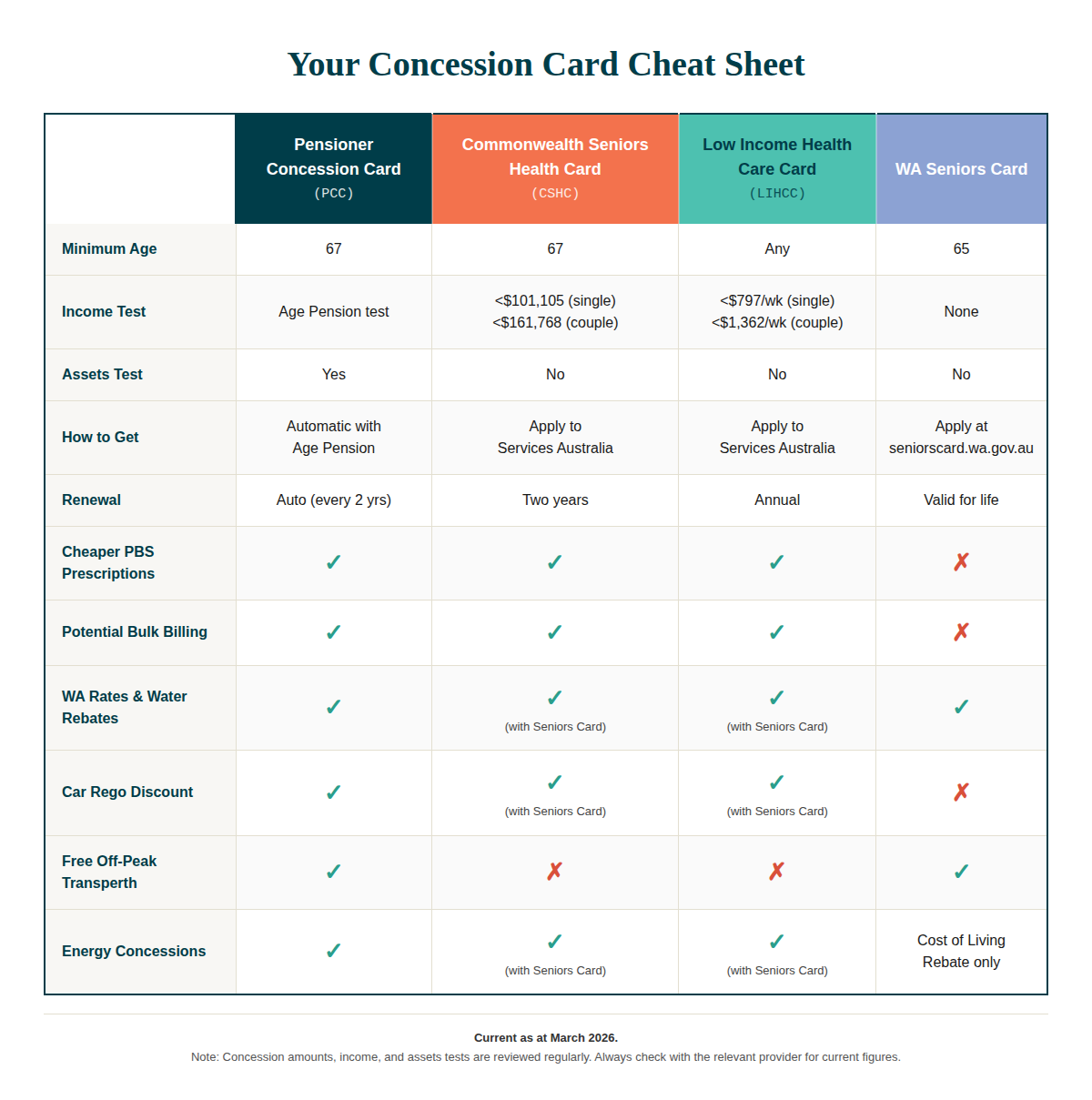

The 4 Concession Cards Every WA Retiree Should Know About

There are four concession cards available to retirees in WA. This guide covers who's eligible, what you get, and how to make the most of them.

If you're retired or getting close, there's a good chance you're entitled to concession cards, government rebates, and benefits you haven't applied for. We see it all the time. People who assume they won't qualify, so they never check.

The Australian concession card system isn't exactly simple. There are multiple cards, each with different eligibility rules, different application processes, and different benefits. Some you get automatically. Others you need to apply for. And you can hold more than one card at the same time.

1. Pensioner Concession Card (PCC)

If you qualify for even one dollar of the Age Pension, you automatically receive a Pensioner Concession Card. You don't need to apply. Services Australia (Centrelink) will post it to you. It's valid for two years and renews automatically as long as you're still eligible.

Who qualifies

Aged 67 or older (Age Pension age)

Meet the Age Pension income and assets tests, even partially

Australian resident living in Australia

What you get in WA

Cheaper PBS prescriptions (substantial savings if you're on regular medications)

Bulk-billed GP visits (at the doctor's discretion, but most will for PCC holders)

Rebates on council rates, water charges, and the Emergency Services Levy

Discounted car registration (up to 50%)

Electricity concessions and the Energy Assistance Payment

Free or concession Transperth travel

Telstra home phone discount

Free or discounted ambulance transport via St John

The PCC is the most comprehensive concession card available.

2. Commonwealth Seniors Health Card (CSHC)

The CSHC is specifically designed for retirees who aren't eligible for the Age Pension, typically because their assets or income are too high. But the income thresholds are more generous than most people realise.

Who qualifies

Aged 67 or older

Not receiving Age Pension or DVA payments

Adjusted Taxable Income under $101,105 (singles) or $161,768 (couples) as at September 2025

No assets test

Australian resident

That last point is critical. There is no assets test for the CSHC. You could have a $2 million home and $3 million in super, and if the income you are drawing from your super and investments is under the threshold, you could still qualify. Many self-funded retirees assume they won't be eligible. But it's assessed on income, not wealth.

What you get

Cheaper PBS prescriptions

Potential bulk-billed GP visits

Extended Medicare Safety Net (lower out-of-pocket threshold)

When combined with a WA Seniors Card: discounts on car registration, rates, water, and energy worth approximately $1,400+ per year in WA

You need to apply. It won't come to you automatically. Apply through Services Australia online or call 132 300.

3. Low Income Health Care Card (LIHCC)

Despite the name, this card isn't only for people on Centrelink payments. The Low Income Health Care Card is available to anyone, at any age, whose income falls below the threshold. For retirees drawing a modest income, it can be genuinely valuable.

Who qualifies

Any age (no minimum age requirement)

Income under approximately $797/week (single) or $1,362/week (couple combined), assessed on the 8 weeks prior to application

No assets test

Australian resident

What you get

Cheaper PBS prescriptions

Potential bulk-billed GP visits

Medicare Safety Net access

In WA, combined with a Seniors Card: access to rate rebates, energy concessions, and car registration discounts

The key difference from the CSHC: income is assessed over 8 weeks (not a full financial year), and it's based on gross income. The card is valid for one year and needs to be renewed annually. If your income fluctuates, the timing of your application matters.

4. WA Seniors Card

The WA Seniors Card is free, there's no income or assets test, and once you get it, it's valid for life. No renewals.

Who qualifies

Aged 65 or older (note: lower than Age Pension age)

Working 25 hours or less per week (averaged over 12 months)

Permanent WA resident (living in WA for more than half the year)

Australian citizen or permanent resident

What you get

Free off-peak Transperth travel (weekdays 9am to 3.30pm and 7pm to 6am, plus weekends and public holidays)

Concession fares at other times

Rebates on council rates and water charges

50% rebate on the Emergency Services Levy

Annual Cost of Living Rebate ($110.07 singles / $165.10 couples)

Discounted entry to Perth Zoo, Art Gallery of WA, Rottnest, national parks and more

Hundreds of business discounts across WA and reciprocal discounts interstate and in NZ

On its own, the WA Seniors Card gives you access to some rebates. But combine it with a CSHC or PCC, and you unlock significantly more, including car registration discounts and bigger rate and energy rebates.

Making the rules work for you

With some careful planning, it's possible to structure your finances in a way that legitimately qualifies you for cards and benefits you might otherwise miss.

One example we see regularly: couples where one partner is older than the other. Say the husband is 68 and the wife is 64. He's already reached Age Pension age; she hasn't. Centrelink assesses a couple's assets jointly, regardless of whose name they're in.

But there's one exception: super in the accumulation phase isn't counted if the owner is under the Age Pension age. By maximising the younger partner's super contributions while she's still under 67, those funds sit outside the means test. The older partner can potentially qualify for a full or higher rate of Age Pension, complete with the Pensioner Concession Card and all its benefits.

Once she reaches Age Pension age, they reassess and restructure again. In the meantime, the family has benefited from pension payments and concessions they were perfectly entitled to, funded by the taxes they've paid for decades.

This isn't gaming the system. It's understanding the rules and making them work for you, which is exactly what a good financial plan should do.

Other strategies might include managing the timing of when you start an account-based pension, choosing which financial year to lodge your CSHC application based on income, or understanding how Centrelink's deeming rules affect your assessed income.

The bottom line

If you're not sure which cards you qualify for, or whether your finances could be structured differently to unlock benefits you're currently missing, get in touch.

Frequently Asked Questions

-

Possibly. The Commonwealth Seniors Health Card has no assets test at all. It doesn't matter how much you have in super, property, or savings. It's assessed purely on income. If your Adjusted Taxable Income is under $101,105 (singles) or $161,768 (couples), you could qualify. We see self-funded retirees with significant wealth qualify for this card all the time.

-

Potentially. Because you haven't reached Age Pension age yet, there are strategies around how your combined assets and income are assessed. Depending on how your finances are structured, your husband may qualify for a part or full Age Pension, which comes with a Pensioner Concession Card. A financial adviser can look at your specific situation and work out the best approach.

-

Not necessarily. Your family home is excluded from the Age Pension assets test. The investment property is counted, but depending on its value and your other assets, you may still qualify for a part pension and the PCC. For the CSHC, assets aren't assessed at all, only income. It's worth getting a financial adviser to run the numbers for your specific situation.

You will qualify for the WA Seniors Card, regardless of whether you qualify for the other concession cards.

-

Yes, and this is one of the most valuable things a financial adviser can do in the lead-up to retirement. The timing of when you start drawing on your super, how your pension is structured, and which financial year you apply in can all affect your eligibility. Getting advice before you retire gives you the best chance of qualifying for the right cards from day one.

-

It depends on your full financial picture. You need to weigh up the rental income, capital gains tax, what you'd do with the proceeds, and how it affects your overall retirement plan.

This is exactly the kind of decision that benefits from proper advice rather than a rule of thumb.

-

You can apply for concession cards at any time, so nothing is permanently lost. But the benefits you could have been receiving over those three years, cheaper prescriptions, rate rebates, car registration discounts, those don't get backdated. The sooner you check your eligibility, the sooner you start saving.

-

It's not too early to plan for them. The decisions you make in the 5 to 10 years before retirement, how much you contribute, which super fund structure you're in, when you start a pension, can directly affect your eligibility for concession cards later. For GESB members in particular, there are specific strategies around preservation age and pension timing that are worth exploring well before you retire.

-

Absolutely. The years leading up to retirement are the best time to structure your finances for maximum benefit. A financial adviser can help you work out which cards you're likely to qualify for, what income and asset thresholds you need to be mindful of, and how to time things like super contributions and pension start dates. Getting this right before you retire means you're not scrambling afterwards.

Join Frankly Speaking

Sign up to receive our monthly newsletter - where the team at Firefly Financial tells it like it is about all things money, life and everything in between.

Sources and Useful Links

Services Australia, Pensioner Concession Card: servicesaustralia.gov.au/pensioner-concession-card

Services Australia, Commonwealth Seniors Health Card: servicesaustralia.gov.au/commonwealth-seniors-health-card

Services Australia, Low Income Health Care Card: servicesaustralia.gov.au/low-income-health-care-card

WA Seniors Card: seniorscard.wa.gov.au

WA Concessions: concessions.wa.gov.au

This information is current as at March 2026. Income thresholds, concession amounts, and eligibility criteria are reviewed and updated regularly by the relevant government bodies. Always check directly with Services Australia or the WA Seniors Card Centre for the most current details before making decisions based on this information.

Kalfocus Pty Ltd AR No. 463978 is a Corporate Authorised Representative of Firefly Financial Pty Ltd AFSL No. 700033, ABN 88 687 477 612. General Advice Warning: Any advice in this article is general advice only and does not take into account the objectives, financial situation or needs of any particular person. It does not represent legal, tax, or personal advice and should not be relied on as such. You should obtain financial advice relevant to your circumstances before making any decisions.